Trading Execution Best Practices: A 2026 Trader's Guide

Trading execution best practices are systematic methods for filling orders at the best available price while controlling costs, risk, and operational error. Regulators including the FCA and frameworks like MiFID II treat best execution not as a courtesy but as a legal obligation. For active traders managing multiple accounts and platforms, the gap between a disciplined execution process and a reactive one shows up directly in P&L. This guide covers what are trading execution best practices, from order type selection and algorithmic strategies to risk discipline and multi-account management.

What are trading execution best practices?

Best execution is defined as the obligation to take all sufficient steps to obtain the best possible result for an order, accounting for price, costs, speed, likelihood of execution, and order size. MiFID II and FCA guidelines codify these factors as the minimum evaluation criteria for every trade. Firms must apply these policies consistently across all client orders and monitor outcomes using Transaction Cost Analysis (TCA).

TCA measures actual fill prices against benchmarks like VWAP (Volume Weighted Average Price) and TWAP (Time Weighted Average Price). The gap between your fill and the benchmark tells you exactly how much your execution process cost you. Without TCA, traders are flying blind on whether their process is working.

Best execution is a governance obligation, not optional. MiFID II and ESMA require integrated TCA and smart order routing infrastructure, reviewed at least annually. Senior management must own the outcome, not just the compliance team.

Pro Tip: Set a monthly TCA review on your calendar. Compare your average fill quality against VWAP for each instrument class. Any consistent negative deviation signals a process problem worth fixing.

The core factors that define execution quality are:

- Price: The fill price relative to the market at the time of order submission

- Costs: Commissions, spreads, and market impact combined

- Speed: Time from order submission to fill confirmation

- Likelihood of execution: Whether the order fills at all, especially for limit orders

- Order size and nature: Large orders require different handling than small retail orders

How do order types and timing strategies impact execution efficiency?

Order type selection is the single most controllable variable in execution quality. Traders who default to market orders in all conditions pay an avoidable cost. Market orders during pre-market and after-hours sessions can carry costs 500 times higher than regular hours, as bid-ask spreads widen from $0.01 to $5.00 or more. That spread difference is a direct tax on impatience.

The Almgren-Chriss model formalizes the core trade-off every trader faces: faster execution increases market impact, while slower execution increases timing risk. Optimal execution speed is determined by risk-aversion models that balance impact cost against exposure to price drift. There is no universally correct answer. The right speed depends on your order size, the instrument’s liquidity, and your risk tolerance.

For large orders, algorithmic slicing is the standard solution. The math is counterintuitive but important: market impact grows with the square root of order size, not linearly. Trading twice the volume costs roughly 1.4 times the impact, not twice. This is why splitting a large parent order into smaller child orders is more cost efficient than sending it all at once.

Algorithmic execution using VWAP or TWAP reduces transaction costs by 20%–40% for orders exceeding 1% of Average Daily Volume. That is a material improvement that compounds over hundreds of trades per month.

The practical steps for applying order timing discipline are:

- Avoid market orders outside regular trading hours. Use limit orders during pre-market and after-hours sessions without exception.

- Classify orders by size relative to ADV. Any order above 1% of ADV warrants algorithmic execution rather than a single market order.

- Choose VWAP for passive participation. VWAP algorithms spread execution across the day proportional to volume, reducing market footprint.

- Choose TWAP for predictable pacing. TWAP works when you want consistent time intervals regardless of volume patterns.

- Apply volatility-based slippage buffers. Dynamic slippage buffers set at 1.5x Average True Range adapt limit order placement to current market conditions and protect against sudden price spikes.

What role do risk management and emotional discipline play in trade execution?

Emotional execution is the most expensive habit in trading. A trader who sizes correctly and follows a plan will outperform a more talented trader who overrides their rules under pressure. Strict risk management limits losses to 0.5%–1% of account equity per trade and prevents the emotional decision-making errors that compound into account-ending drawdowns.

Stop-loss orders placed at technical levels are the mechanical enforcement of that limit. They remove the in-the-moment decision of when to exit a losing trade. Without a hard stop, traders routinely hold losers too long, hoping for a reversal that statistically does not come.

Overtrading and emotional executions stem from structural failures in the trading process, not character flaws. Repeatable systems with pre-session checklists and equity-curve-based position sizing reduce these lapses. The checklist forces a deliberate review before any capital is at risk.

Pro Tip: Build a pre-session checklist that covers your max daily loss limit, the instruments you will trade, and your position sizing formula. Review it before placing your first order every single day.

The structural rules that support execution discipline include:

- Daily loss limits: Define the maximum drawdown that triggers a trading halt for the day

- Trade count limits: Cap the number of trades per session to prevent overtrading after losses

- Equity-curve sizing: Reduce position size when your account equity is below its moving average

- Defined entry and exit criteria: Active trading plans with explicit criteria reduce emotion and let you track decision quality separately from P&L

The goal is to make good execution the default, not the exception. Systems do that. Willpower alone does not.

How can traders optimize execution across multiple platforms and accounts?

Managing execution across multiple platforms multiplies every risk that exists on a single account. Order duplication, inconsistent sizing, and missed fills on one account while another fills correctly are all real failure modes. The solution is centralized execution logic with account-level controls applied at the point of order generation.

Smart order routing (SOR) addresses the venue selection problem. When the same instrument trades on multiple venues, SOR evaluates available liquidity and routes the order to the best available price. Large orders can be routed via parallel or sequential routing, each with distinct trade-offs. Parallel routing captures fleeting liquidity across venues simultaneously but risks overfilling. Sequential routing is less visible to the market but risks liquidity disappearing before the order completes.

The table below compares the two primary routing approaches for multi-venue execution:

| Routing method | Best use case | Primary risk |

|---|---|---|

| Parallel (spraying) | Fast-moving markets with fragmented liquidity | Overfilling across venues |

| Sequential | Stealth execution for large orders | Liquidity vanishing before completion |

| Algorithmic (VWAP/TWAP) | Large orders relative to ADV | Timing risk over extended execution window |

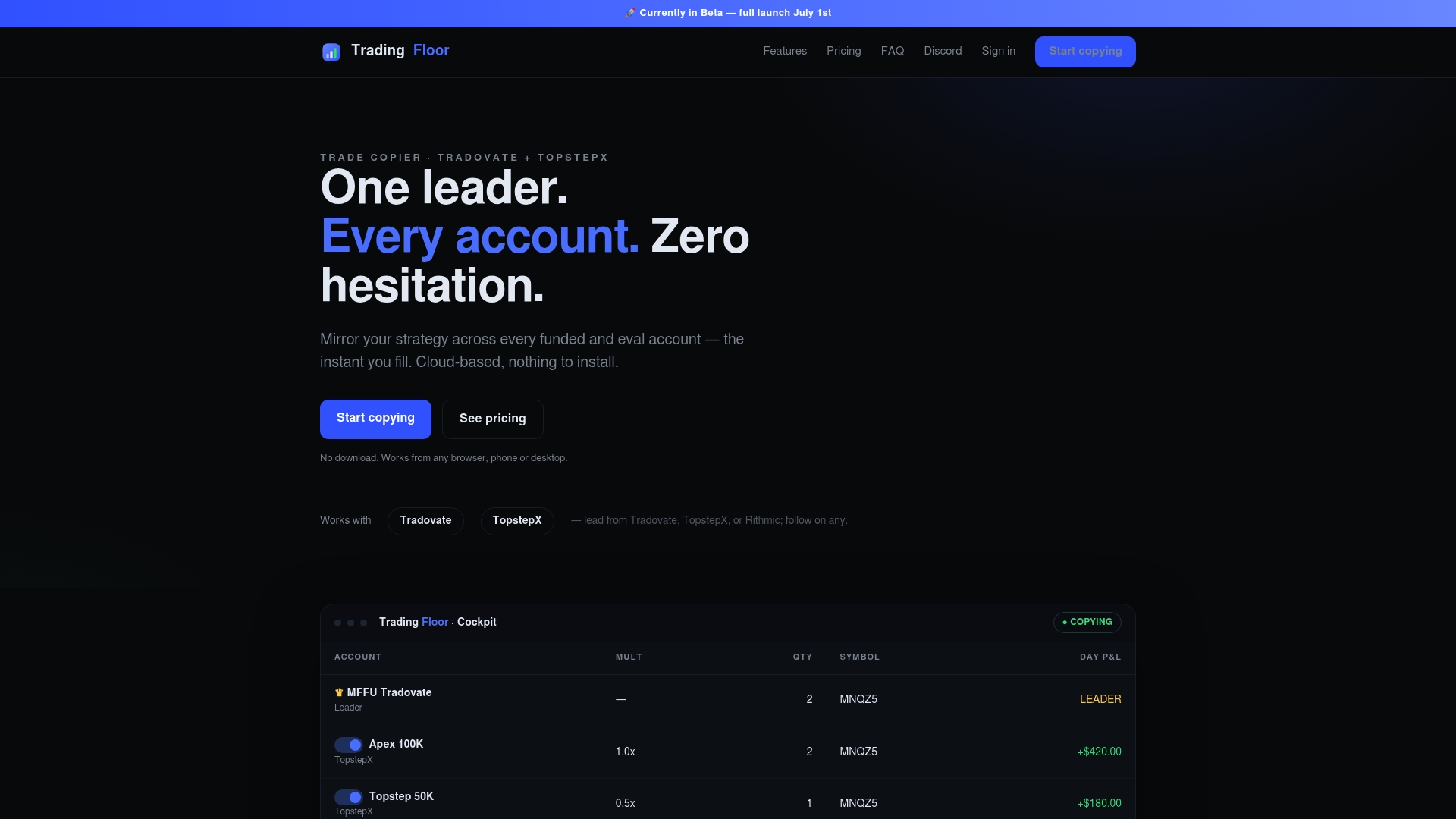

For prop traders running funded and evaluation accounts simultaneously, the execution challenge is consistency. A fill on the leader account must translate correctly to every follower account without manual intervention. Manual replication across accounts creates latency, sizing errors, and missed trades. Tradingfloor addresses this by mirroring real-time positions across multiple accounts, copying the leader’s net position rather than just signals, with individual risk controls applied per account.

Traders managing multiple broker platforms also face the risk of strategy drift, where the same setup produces different results on different platforms due to order routing differences, latency, or margin rules. Standardizing your execution process at the strategy level, not the platform level, is the fix.

Key Takeaways

Disciplined trade execution requires combining regulatory-grade monitoring, algorithmic order management, and structural risk rules into one repeatable process.

| Point | Details |

|---|---|

| Define best execution criteria | Evaluate every order on price, cost, speed, fill likelihood, and order size per MiFID II standards. |

| Use TCA benchmarks | Measure fills against VWAP or TWAP monthly to identify and fix execution gaps. |

| Apply algorithmic slicing | Use VWAP or TWAP algorithms for orders above 1% of ADV to cut transaction costs by 20%–40%. |

| Cap risk per trade | Limit losses to 0.5%–1% of account equity per trade and use hard stop-loss orders at technical levels. |

| Centralize multi-account execution | Use position mirroring rather than manual replication to maintain consistency across accounts and brokers. |

What I’ve learned from watching traders ignore their own execution rules

Most traders spend 90% of their preparation time on trade selection and about 10% on how they will actually execute. That ratio is backwards. I have watched traders with genuinely good setups lose money consistently because their execution process was reactive and inconsistent.

The insight that changed how I think about this: execution quality is a separate skill from market analysis. A trader can read the market correctly and still lose money if they enter at the wrong time, use the wrong order type, or size incorrectly. These are process failures, not analytical failures.

The traders I have seen improve fastest are the ones who treat their execution log as seriously as their trade journal. They record fill price versus intended price, note the order type used, and track slippage over time. That data tells you where your process is leaking money. Without it, you are guessing.

Speed is also more dangerous than most traders admit. The instinct to get filled immediately costs real money in market impact and spread. Slowing down, using limit orders, and letting the market come to you is uncomfortable. It feels like you are missing the trade. But the data consistently shows it produces better fills over a large sample.

The best execution process is one you will actually follow under pressure. Simple, documented, and reviewed regularly.

— KennyTrades

How Tradingfloor supports best execution across every account

Executing a disciplined process on one account is hard enough. Doing it consistently across multiple funded and evaluation accounts simultaneously is where most prop traders lose ground.

Tradingfloor is built for exactly this problem. It mirrors the leader account’s real-time net position across every connected account on platforms including Tradovate and TopstepX, with individual risk controls applied per account. There is no manual replication, no latency from copying signals, and no risk of order duplication. Traders get centralized execution control with account-level guardrails that enforce the risk limits covered in this guide. If you are managing more than one account and still executing manually, review Tradingfloor’s pricing plans to see how the platform fits your current setup.

FAQ

What is best execution in trading?

Best execution is the obligation to take all sufficient steps to obtain the best possible result when filling an order, evaluated on price, cost, speed, and likelihood of execution. MiFID II and FCA guidelines make this a regulatory requirement for firms, not a discretionary standard.

When should traders use limit orders instead of market orders?

Traders should use limit orders during pre-market and after-hours sessions, and for any order that represents more than 1% of a stock’s Average Daily Volume. Market order costs outside regular hours can be 500 times higher due to widened bid-ask spreads.

What is VWAP and why does it matter for execution?

VWAP is the Volume Weighted Average Price, a benchmark that measures whether your fills are better or worse than the average price weighted by volume throughout the day. Algorithmic execution targeting VWAP reduces transaction costs by 20%–40% for large orders.

How much risk should a trader take per trade?

The standard risk management guideline caps losses at 0.5%–1% of account equity per trade. This limit, enforced with hard stop-loss orders, prevents single trades from causing account-level damage and removes emotional exit decisions.

How do you manage execution across multiple trading accounts?

The most reliable method is position mirroring, where a leader account’s net position is automatically replicated across follower accounts with individual risk controls. Manual replication creates latency and sizing errors that compound across accounts.

Recommended

- Multi-Platform Trading Best Practices for Prop Traders — Trading Floor

- Trade the Same Strategy Across Multiple Brokers — Trading Floor

- Trading Performance Review: A Complete 2026 Guide — Trading Floor

- Multi-Account Trade Execution Explained for Prop Traders — Trading Floor

Trading Floor mirrors every trade across your Tradovate, TopstepX & Rithmic accounts in real time, from $25/mo.

Start copying →