Net Position Tracking in Trading: A 2026 Guide

Net position tracking is defined as the consolidation of all long and short positions in the same instrument into a single exposure metric that reveals a trader’s true market risk. The role of net position tracking in trading goes far beyond bookkeeping. It determines whether you are actually exposed to the market the way you think you are. The CFTC Commitments of Traders (COT) report publishes weekly net speculative positions for instruments like S&P 500 E-mini futures, and those numbers swing by hundreds of thousands of contracts. That scale shows how much institutional sentiment shifts week to week, and why tracking your own net exposure with the same discipline matters.

What is the role of net position tracking in trading?

Net position tracking gives traders a single, honest number: the difference between total long contracts and total short contracts in a given instrument. Without it, you can hold offsetting trades across accounts and believe you are hedged when you are actually doubling your exposure. The importance of position tracking becomes obvious the moment you run two accounts on the same futures contract without a consolidated view.

Position netting matches buy and sell positions in the same instrument and account to reduce the total market exposure visible on your monitor. This is not just a display preference. It is the foundation of accurate risk accounting. Traders who skip this step routinely misread their real dollar exposure, especially when scaling into positions across multiple entries.

The COT report is the institutional version of this practice. Regulators require large traders to report net positions weekly, and that data becomes a sentiment indicator for the entire market. Retail traders who apply the same netting logic to their own books gain the same structural clarity that institutions use to make high-conviction decisions.

How does net position tracking work for equity and futures traders?

The mechanics of net position tracking center on two processes: netting and reconciliation. Netting collapses opposite trades into one number. Reconciliation confirms that number matches reality by comparing your internal portfolio state against broker API data.

![]()

Real-time synchronization between local portfolio states and broker APIs prevents position drift, which is the gradual divergence between what your system thinks you hold and what the broker actually shows. Reconciliation systems typically run every 5 minutes, and the best ones track maximum adverse excursion (MAE) on every tick to sharpen stop-loss placement. That frequency matters in fast markets where a 5-minute gap can mean a missed stop.

Consider a practical example. You are trading S&P 500 E-mini futures. You enter long 3 contracts at the open, then short 1 contract as a hedge 20 minutes later. Your net position is long 2 contracts, not long 3 and short 1 separately. If your tracking system does not consolidate those trades, your risk model overstates your gross exposure and may trigger unnecessary margin alerts.

Common pitfalls in this process include:

- Exposure drift: Your local state diverges from the broker’s record due to asynchronous data feeds.

- Unauthorized leverage: Gross positions appear larger than net positions, masking actual risk until a reconciliation failure surfaces.

- Execution delays: A filled order that arrives late in your system creates a phantom position that distorts P&L calculations.

- Missed stop losses: Without tick-level MAE tracking, stop-loss levels are placed on averages rather than actual worst-case drawdowns.

Pro Tip: Set your reconciliation interval to 5 minutes or faster and log every discrepancy between your local state and the broker API. Those logs are your early warning system for drift before it becomes a loss.

What role do net delta and option Greeks play in position tracking?

Options traders face a more complex version of net position analysis in trading because each contract carries directional exposure that changes with price, time, and volatility. Net delta is the aggregate directional bias of an options portfolio after all positions are summed. It tells you whether your book profits from a move up or down in the underlying.

Market makers hedge delta exposure by buying or selling the underlying asset, and understanding their net delta reveals whether the market needs to buy or sell to stay balanced. When dealers are net long delta, customers are net short and must buy the underlying to hedge. That buying pressure becomes a structural tailwind for price. Ignoring dealer delta flows means missing one of the most consistent drivers of short-term price direction.

The other Greeks add layers of precision:

- Gamma measures how fast delta changes as price moves. High net gamma near a strike means small price moves create large hedging demands, which accelerates price movement.

- Vanna tracks how delta changes with implied volatility. A volatility spike forces dealers to rehedge, creating directional flows that look random without this context.

- Charm measures how delta decays with time. As expiration approaches, charm-driven flows intensify, especially in the final hours of an options cycle.

- Net gamma inflection points mark price levels where dealer hedging switches from stabilizing to destabilizing. Crossing these levels often triggers the sharp moves traders call breakouts.

Options expiration events cause rapid dealer delta position shifts. After expiry, delta hedges unwind and push prices in the opposite direction of the prior delta bias. Traders who track net delta into expiration can anticipate these reversals rather than react to them.

Why is net position tracking essential for risk management?

Position managers function as accounting systems. They separate unrealized P&L from realized P&L, which is the single most important distinction in disciplined trading. Without accurate position management, traders risk flying blind, missing stop losses, and letting small losses compound into large ones.

The emotional dimension is real. A trader watching an unrealized loss often treats it differently than a realized one. Accurate position tracking removes that ambiguity. The number on your screen reflects actual exposure, not a story you are telling yourself about where the trade might go.

Key risk management functions that depend on accurate position tracking:

- Unrealized vs. realized P&L separation: Prevents traders from counting paper gains as spendable capital.

- Per-account visibility: Granular per-exchange tracking identifies drift and P&L errors that aggregate views hide entirely.

- MAE-based stop placement: Maximum adverse excursion data from tick-level tracking shows the worst drawdown a trade experienced, giving you a data-driven basis for stop-loss levels rather than guesswork.

- Margin conflict detection: Storing only net positions masks execution delays and margin conflicts across accounts.

Pro Tip: Review your MAE data weekly. If your stops are consistently tighter than your average MAE, you are getting stopped out by noise. Widen them to the level your actual trade history supports.

How can traders apply position tracking across multiple accounts?

Managing multiple accounts without a consolidated dashboard is the fastest way to accumulate hidden exposure. Each account looks fine in isolation. Together, they may be massively overweight one direction without any single account showing a red flag.

The solution is cross-venue inventory management: a single view that aggregates net positions across all accounts and brokers in real time. Reconciling WebSocket streams and REST API data maintains state accuracy across venues, but the systems must handle asynchronous data without creating phantom positions or missing fills.

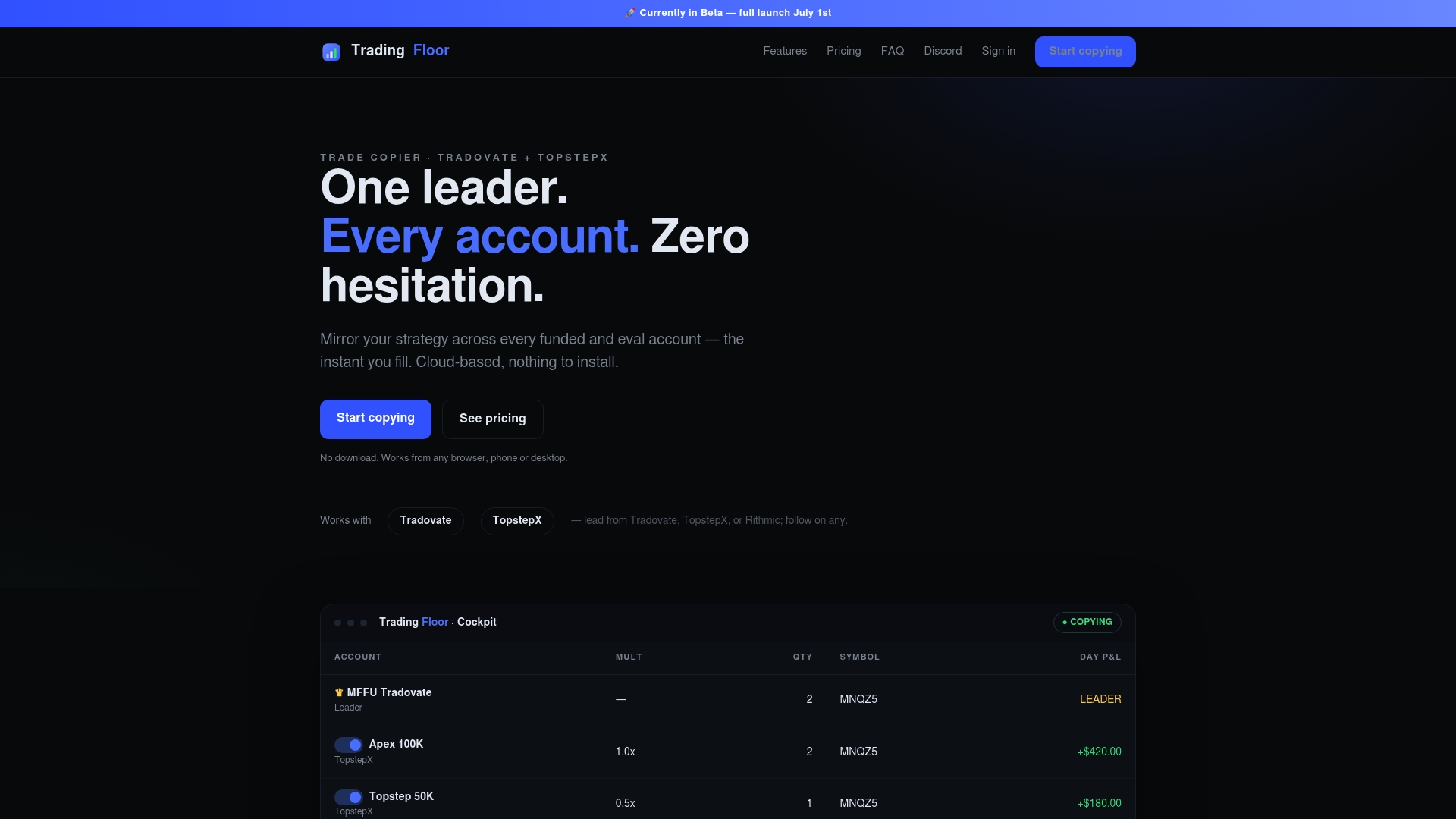

Prop traders face this challenge acutely. A trader running three funded accounts on the same futures instrument needs to know the combined net position, not three separate numbers. If account A is long 2, account B is long 1, and account C is short 1, the net exposure is long 2. Without that consolidated view, the trader may add to account B thinking they are underexposed when they are already at their intended size.

Institutional signal convergence raises conviction levels for position traders by combining COT data, SEC 13F filings, and insider trade reports into a single directional thesis. The same logic applies at the account level. Convergence of position data across accounts gives you a cleaner read on your actual market stance than any single account view provides.

Tradingfloor addresses this directly. It mirrors the leader’s net position across funded and evaluation accounts in real time, with individual risk controls applied per account. Traders on platforms like Tradovate and TopstepX can synchronize positions without manual reconciliation, which eliminates the execution errors that come from managing accounts separately.

Key Takeaways

Net position tracking is the foundation of accurate risk management, and traders who skip it are working with incomplete information regardless of how good their entry signals are.

| Point | Details |

|---|---|

| Net position defined | Subtract total short contracts from total long contracts in the same instrument to get true exposure. |

| Reconciliation frequency | Systems should reconcile broker API data against local state every 5 minutes or faster to prevent drift. |

| Dealer delta flows | Tracking net delta reveals whether market makers need to buy or sell, which drives short-term price direction. |

| MAE for stop placement | Maximum adverse excursion data from tick-level tracking gives a data-driven basis for stop-loss levels. |

| Multi-account consolidation | A single consolidated dashboard prevents hidden overexposure when running multiple funded accounts simultaneously. |

Why I think most traders underestimate position tracking

Most traders treat position tracking as a back-office function. They focus on entries, setups, and signals, then assume the accounting side takes care of itself. That assumption is expensive.

The traders I have seen manage multiple funded accounts successfully all share one habit: they check their consolidated net position before they add any new trade. Not the individual account. The total. That discipline alone prevents the most common multi-account mistake, which is accidentally doubling a position you thought you were hedging.

The institutional angle is equally underappreciated. Dealer delta flows and COT positioning are not abstract concepts. They are the actual buying and selling pressure that moves prices at key levels. A trader who tracks net delta into an options expiration is not guessing at the reversal. They are reading the structural demand that will force market makers to unwind hedges. That is a different quality of information than a candlestick pattern.

Real-time tracking also changes your relationship with losing trades. When you can see exactly what you hold, what it cost, and what the unrealized P&L is at every moment, the emotional pull to hold a loser weakens. The number is the number. There is no narrative to hide behind. That clarity is worth more than most traders realize until they have traded without it.

Fast markets in 2026 make all of this more urgent. Execution speeds have increased, and the window between a missed reconciliation and a real loss has narrowed. Traders who rely on end-of-day position reviews are operating on yesterday’s data in a market that moves in seconds.

— KennyTrades

Tradingfloor: one view for all your accounts

Prop traders managing multiple funded accounts need more than a good strategy. They need a system that keeps every account in sync without manual intervention.

Tradingfloor mirrors the leader’s net position across all your funded and evaluation accounts in real time. No manual reconciliation. No position drift. Each account keeps its own risk controls while the leader’s trades copy automatically. The platform runs in the cloud, so there is nothing to install and it works from any device. Whether you trade on Tradovate or TopstepX, Tradingfloor keeps your multi-account positions aligned and your exposure visible at a glance. Check the pricing options to find the plan that fits your account structure.

FAQ

What is net position tracking in trading?

Net position tracking is the process of consolidating all long and short positions in the same instrument into a single exposure number. It shows your true market risk rather than gross position size.

How often should position reconciliation run?

Reconciliation should run every 5 minutes at minimum, with tick-level MAE tracking for stop-loss optimization. Faster intervals reduce the risk of position drift in volatile markets.

Why does net delta matter for options traders?

Net delta reveals whether market makers need to buy or sell the underlying to stay hedged, which creates directional price pressure. Tracking dealer net delta helps traders anticipate price moves rather than react to them.

How does net position tracking help with multiple accounts?

A consolidated dashboard shows the combined net exposure across all accounts, preventing accidental overexposure when the same instrument is held in multiple funded accounts simultaneously.

What is maximum adverse excursion and why does it matter?

Maximum adverse excursion (MAE) measures the worst drawdown a trade experienced during its life cycle. Tracking MAE on tick data gives traders a factual basis for setting stop-loss levels instead of relying on arbitrary distances from entry.

Recommended

Trading Floor mirrors every trade across your Tradovate, TopstepX & Rithmic accounts in real time, from $25/mo.

Start copying →