Account-Level Risk Management: A Trader's Complete Guide

Account-level risk management is defined as the micro-level process of monitoring and controlling risks tied to individual trading or investment accounts, where exposure is generated at the point of trade execution. Known formally as Micro Level risk management, it operates at the operational layer of a firm’s risk structure, distinct from board-level strategy or business-line oversight. Traders who understand this discipline gain a concrete edge: they can enforce position limits, detect behavioral deviations early, and keep every account aligned with predefined risk parameters. This guide breaks down the full framework, from risk scoring to dynamic controls to enterprise integration.

What is account-level risk management and why does it matter?

Account-level risk management is the practice of evaluating and controlling the specific risks that exist within a single trading or investment account. It sits at the bottom of a three-tier risk structure that includes strategic, macro, and micro-level oversight. At this level, front-line traders and compliance officers enforce operational guidelines to keep exposures within board-approved limits.

The distinction from higher-level risk management is critical. Strategic risk management sets the firm’s overall risk appetite. Macro-level management governs business lines and product categories. Account-level risk management translates those policies into specific, enforceable controls on individual accounts. Without this translation, board-approved limits remain abstract targets with no operational teeth.

For traders managing multiple funded accounts, this matters immediately. A single account breaching its drawdown limit can trigger a firm-wide review, a funded account termination, or a regulatory flag. Account-level controls are the last line of defense before those consequences materialize.

What factors are evaluated in account risk assessment?

Account risk assessment draws on multiple data points to produce a composite risk rating for each account. No single factor determines risk. Instead, a weighted scorecard approach assigns numerical values to each input and combines them into a single score.

Weighted scorecard models typically distribute weights across four core factors:

- Geographic risk: The jurisdiction where the account operates, accounting for regulatory environment and financial crime exposure.

- Customer type: Whether the account holder is a retail trader, institutional investor, or politically exposed person.

- Product risk: The complexity and volatility of instruments traded, such as futures, options, or leveraged ETFs.

- Behavioral factors: Transaction frequency, size patterns, and deviations from the account’s established trading profile.

A common weighting structure assigns 30% to geographic risk, 25% to customer type, 20% to product risk, and 25% to behavioral factors. That distribution reflects the reality that behavior and geography together drive more than half the composite score. The resulting rating determines the intensity of monitoring applied to that account.

| Risk Factor | Typical Weight | What It Captures |

|---|---|---|

| Geographic risk | 30% | Jurisdiction, regulatory environment |

| Customer type | 25% | Retail, institutional, PEP status |

| Behavioral factors | 25% | Transaction patterns, frequency, size |

| Product risk | 20% | Instrument complexity, leverage level |

These scores are not static. An account that begins trading a new leveraged product, or suddenly increases transaction frequency, should trigger a score recalculation. The composite rating directly influences how often the account is reviewed and what controls are applied.

How do traders apply account-level risk controls to manage exposure?

Risk controls at the account level fall into three categories: preventive, detective, and reactive. Preventive controls stop a risk event before it occurs. Detective controls identify a risk event as it happens. Reactive controls limit damage after an event has taken place. Effective account management uses all three in sequence.

The hierarchy of controls framework provides a practical structure for prioritizing these measures. Engineering or structural controls are more effective than administrative procedures because they remove the possibility of human error. For traders, a structural control is a hard position limit enforced by the platform. An administrative control is a policy requiring manual review before a large trade. The structural limit is more reliable.

Here is how traders typically layer controls at the account level:

- Set hard position limits. Define the maximum notional exposure allowed per instrument and per account. These limits enforce themselves without requiring human intervention.

- Establish daily loss thresholds. A maximum daily drawdown triggers an automatic halt or alert before the account reaches its funded account breach level.

- Apply product-specific restrictions. Accounts with lower risk scores may be restricted from trading highly leveraged or complex instruments until the profile warrants access.

- Monitor behavioral deviations in real time. Automated alerts fire when transaction size, frequency, or timing falls outside the account’s established pattern.

- Require manual review for edge cases. When behavior deviates beyond expected profiles even if scores appear acceptable, manual investigation catches emerging risks that automated scoring misses.

Pro Tip: Never treat a risk control as purely risk-reducing. Some controls shift risk from one form to another. A hard daily loss limit prevents a catastrophic drawdown but may push a trader toward over-concentration in fewer positions to recover losses faster. Audit your controls for unintended consequences quarterly.

Regulated environments add another layer. Before applying any control, account appropriateness must be confirmed. This means verifying that the account structure matches the client’s goals, risk tolerance, and risk capacity. A trader with a conservative risk profile should not hold an account configured for aggressive leveraged trading, regardless of their score.

How does account structure, product complexity, and risk oversight interact?

Account structure, product complexity, and business line do not add risk together. They multiply it. This is the concept of the risk stack, and it is one of the most underappreciated ideas in financial risk management.

A margin account holding plain equity positions carries moderate risk. The same margin account holding leveraged futures contracts carries substantially higher risk. Add a business line that processes high-frequency trades across multiple jurisdictions, and the combined risk profile is far greater than any single factor suggests. Each layer amplifies the others.

| Account Type | Product Complexity | Risk Stack Level | Oversight Required |

|---|---|---|---|

| Cash account | Low (equities) | Low | Standard monitoring |

| Margin account | Medium (options) | Elevated | Enhanced review |

| Margin account | High (leveraged futures) | High | Approval and daily oversight |

| Multi-account structure | High (cross-product) | Very high | Integrated supervision |

The practical implication is that isolated risk views fail. Reviewing account structure alone, or product risk alone, produces an incomplete picture. Supervisors and traders must assess the full stack together before approving account configurations or new product access.

For prop traders running multiple funded accounts, this is especially relevant. Each account may appear compliant in isolation. But if all accounts hold correlated leveraged positions, the aggregate exposure creates a risk stack that no single account review would catch. Integrated supervision across accounts is not optional at that point. It is the only way to see the real exposure.

How does account-level risk management fit within enterprise risk frameworks?

Enterprise risk management operates across three levels simultaneously. The board sets risk appetite and approves limits at the strategic level. Business line managers enforce those limits across product categories at the macro level. Front-line traders and compliance officers apply them to individual accounts at the micro or operational level.

Account-level controls are the mechanism that connects board policy to actual trading behavior. Without them, a firm’s stated risk appetite has no operational enforcement. With them, every trade executed at the account level either stays within approved parameters or triggers a review.

The coordination between levels requires clear communication in both directions:

- Downward: Board-approved limits translate into specific account thresholds, position caps, and product restrictions.

- Upward: Account-level data feeds into business-line and enterprise risk reports, giving senior management visibility into where exposure is accumulating.

- Lateral: Account-level risk data informs compliance teams monitoring for regulatory flags, AML triggers, and suitability violations.

Continuous monitoring is the operational requirement that makes this coordination work. Static annual reviews miss the behavioral shifts and market condition changes that create risk between review cycles. Dynamic risk controls that adjust to portfolio changes and market conditions are the standard for any account-level risk program worth running.

Key Takeaways

Account-level risk management is the operational layer where board-approved limits become enforceable controls on individual trading accounts, using weighted scoring, structural limits, and continuous monitoring to keep exposure within defined parameters.

| Point | Details |

|---|---|

| Micro-level definition | Account-level risk management enforces board-approved limits at the individual account and trade execution level. |

| Weighted risk scoring | Composite scores combine geographic, customer, product, and behavioral factors to set monitoring intensity. |

| Risk stack concept | Account structure, product complexity, and business line multiply risk rather than add it, requiring integrated oversight. |

| Control hierarchy | Structural controls like hard position limits outperform administrative procedures because they remove human error. |

| Dynamic adjustment | Static controls create blind spots; risk limits must update when market conditions or account behavior changes. |

Why most traders get account-level risk wrong

Most traders treat risk controls as a one-time setup task. They set a daily loss limit, configure a position cap, and move on. That approach works until market conditions shift or trading behavior evolves, and then the static controls become a false sense of security.

The insight that changed how I think about this: controls modify risk, they do not simply reduce it. A hard daily loss limit prevents a blowup, but it can also push a trader into riskier recovery behavior within the same session. Recognizing that dynamic means you audit your controls for second-order effects, not just first-order protection.

The other mistake I see constantly is over-reliance on automated scoring. Automated scores are a baseline. They reflect historical behavior. They do not catch the trader who is slowly increasing position size each week in a way that looks normal until it does not. That is exactly the scenario where manual review catches what the algorithm misses.

The traders who handle account-level risk well share one habit: they treat their risk framework as a living document. They review their composite risk scores when they add a new product. They recalibrate their position limits when their account balance changes materially. They check whether their account structure still matches their actual trading goals every quarter. That discipline is not complicated. It is just consistent.

— KennyTrades

How Tradingfloor supports account-level risk control

Prop traders managing multiple funded accounts face a specific version of the risk stack problem: each account looks fine in isolation, but the aggregate exposure across accounts is invisible without the right tools.

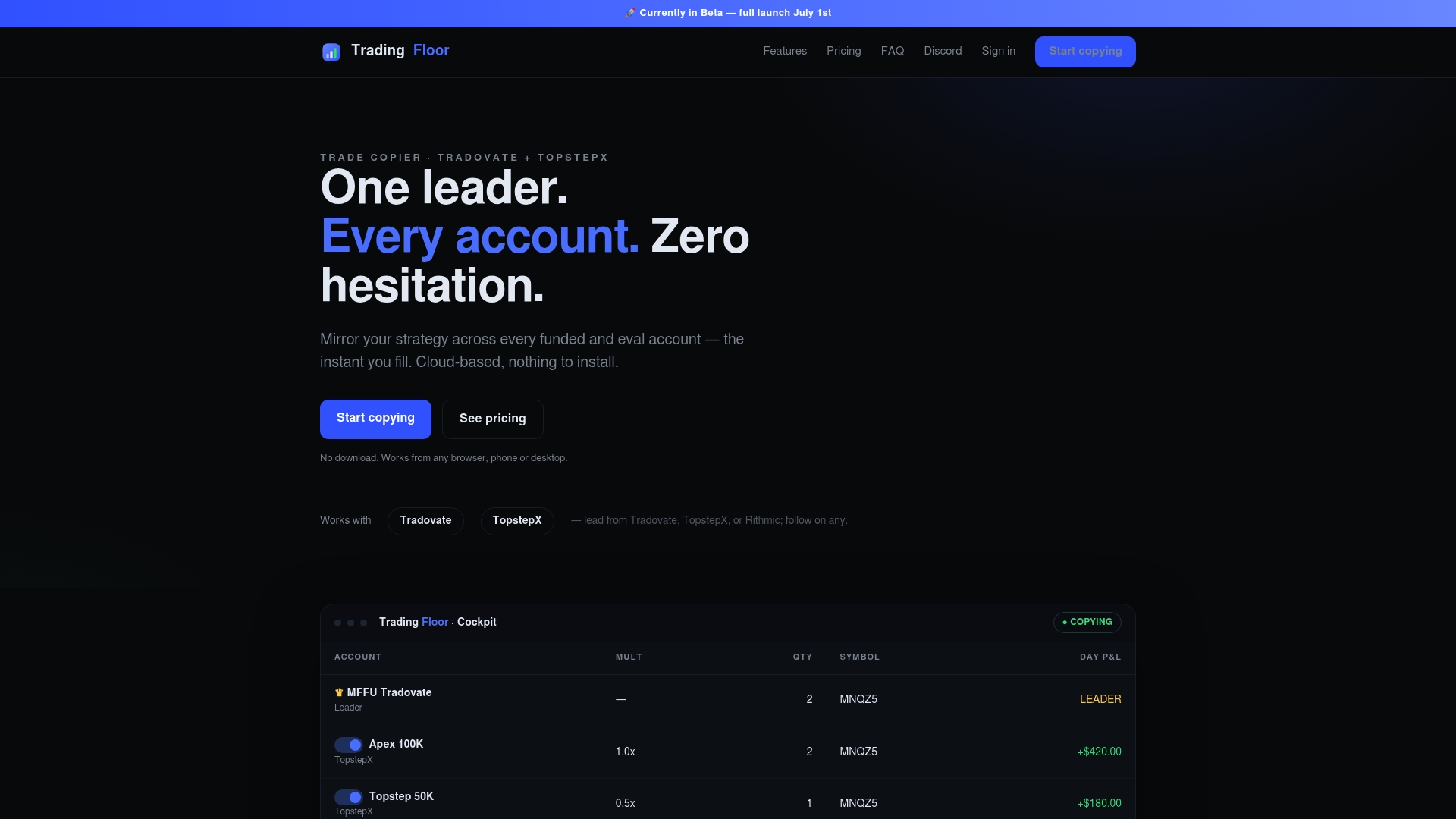

Tradingfloor addresses this directly. The platform mirrors a leader account’s net position across funded and evaluation accounts in real time, while maintaining individual risk controls on each account. Trade limits and real-time notifications enforce account-level thresholds without requiring manual intervention on every position. Traders using Tradovate and TopstepX can manage cross-account exposure from any device without installing software. For traders who want to see how the account management platform fits their current risk setup, Tradingfloor’s full feature set and pricing options are available on the site.

FAQ

What is account-level risk management?

Account-level risk management is the micro-level process of monitoring and controlling risks within individual trading or investment accounts. It enforces board-approved limits through operational controls applied at the point of trade execution.

How is account risk scored?

Account risk is scored using a weighted scorecard that combines geographic risk, customer type, product complexity, and behavioral patterns into a composite rating. That rating determines the level of monitoring and controls applied to the account.

What is the difference between risk tolerance and account appropriateness?

Risk tolerance is the degree of loss a client is willing to accept. Account appropriateness assesses whether the account structure and products within it actually match that tolerance and the client’s financial goals.

Why does the risk stack concept matter for prop traders?

Prop traders running multiple accounts with correlated leveraged positions face multiplicative risk, not additive risk. No single account review reveals the true aggregate exposure, which is why integrated supervision across all accounts is required.

When should automated risk scores be supplemented with manual review?

Automated scores should trigger manual review when account behavior deviates from established patterns, even if the score itself remains within acceptable range. Early behavioral shifts are the leading indicator of emerging risk that algorithms typically miss.

Recommended

Trading Floor mirrors every trade across your Tradovate, TopstepX & Rithmic accounts in real time, from $25/mo.

Start copying →